Non-Resident Tax Filing Services

We prepare Canadian and U.S. non-resident tax filings for individuals with income, property, residency changes, or filing obligations across the border.

Non-resident tax filing can arise when a person earns income in a country where they do not live. It can also arise in the year a person moves to or from the United States or Canada.

As a result, the correct filing approach may require both residency analysis and source-of-income analysis. In addition, the filing may involve federal, provincial, state, treaty, withholding, or foreign reporting issues.

Need help with a non-resident tax filing?

We can help identify whether a Canadian or U.S. non-resident return is required. We also review withholding and treaty issues and prepare a coordinated filing plan.

What Is a Non-Resident Tax Filing?

A taxpayer may need a non-resident tax filing when they have income connected to a country where they do not live as a tax resident. In some cases, the payer withholds tax at source. However, the taxpayer may still need or benefit from filing a return.

For example, a Canadian living in the United States may have a Canadian filing obligation if they still earn Canadian-source income. Similarly, a Canadian resident may need a U.S. non-resident return if they have certain U.S.-source income.

Who May Need a Non-Resident Tax Return?

Non-resident tax filing obligations depend on residency, income type, source of income, treaty rules, and withholding. Therefore, the correct filing position depends on the facts.

- Canadians who moved to the United States

- U.S. residents with Canadian-source income

- Non-residents with Canadian rental income

- Non-residents receiving Canadian pension or retirement income

- Canadians with U.S.-source rental income

- Canadians who need to file Form 1040-NR

- Individuals who moved to or from the United States during the year

- Taxpayers with provincial, state, or dual-status filing issues

Canadian Non-Resident Tax Filings

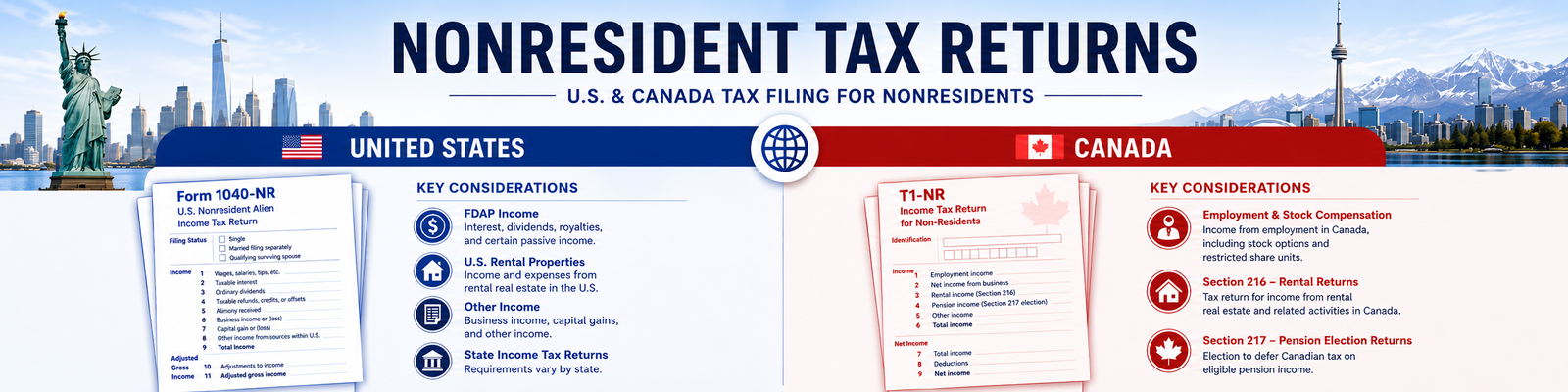

Canada taxes individuals based on both residency and source of income. Therefore, a person who becomes a non-resident of Canada may still have Canadian filing obligations if they continue to earn Canadian-source income.

Canadian non-resident income often falls into different categories. Some income may require an annual Canadian non-resident return. Other income may be subject to Canadian non-resident withholding tax.

Part I Canadian Tax

Part I tax may apply to income such as Canadian employment income, business income, and taxable capital gains from certain Canadian property. In many cases, the taxpayer files an annual Canadian return to calculate the final tax obligation.

Part XIII Canadian Withholding Tax

Part XIII tax may apply to dividends, rents, royalties, pensions, RRSP or RRIF payments, and certain other amounts paid to non-residents. The payer often withholds tax at a default rate of 25%, unless a treaty reduces the rate.

Section 216 Rental Elections

A Section 216 return may allow a non-resident landlord to report Canadian rental income on a net-income basis. As a result, the taxpayer may avoid tax based only on gross-rent withholding.

Section 217 Pension Elections

A non-resident may be able to file a Section 217 return for certain Canadian pension, retirement, or benefit income. In some cases, it can reduce the final Canadian tax cost compared with withholding alone.

Provincial tax or non-resident surtax can also matter. For example, employment income earned while working in Canada may create provincial tax in the province where the work was performed.

In other cases, a federal non-resident surtax may apply. Therefore, the return should be reviewed based on the type of income and where the income was earned.

Canadians Living in the United States

Canadians who move to the United States may not have an ongoing Canadian resident tax filing obligation after they become non-residents of Canada. However, the year of departure often requires careful Canadian reporting.

After departure, Canadian filing requirements usually depend on whether the person still has Canadian-source income. For example, Canadian rental property, Canadian pensions, Canadian employment income, or certain dispositions of Canadian property may still create filing or withholding issues.

Canadian tax residence depends on the specific facts. In addition, treaty rules may need to be reviewed if both countries could treat the person as resident under domestic law.

Americans Living in Canada

U.S. citizens and green card holders generally remain subject to U.S. tax filing rules even while living in Canada. As a result, they often file full U.S. resident returns rather than U.S. non-resident returns.

This means that a U.S. citizen or green card holder living in Canada may need to file Form 1040, report worldwide income, and review foreign account reporting. These obligations are different from the Form 1040-NR rules that apply to non-resident aliens.

Learn more about U.S. tax filing services and foreign account and asset reporting.

U.S. Non-Resident Tax Filings for Canadians

U.S. non-resident federal tax filings generally apply to non-resident aliens who have certain types of U.S.-source income. Taxpayers commonly report this income on Form 1040-NR.

U.S.-source income can include employment income, business income, rental income, certain pension or retirement payments, and fixed or determinable annual or periodic income. This last category is commonly called FDAP income.

FDAP Income

FDAP income can include interest, dividends, rents, royalties, and similar income. The default U.S. withholding rate is often 30%, unless a treaty reduces the rate.

U.S. Rental Property

A Canadian with U.S. rental property may be able to elect to report rental income on a net-income basis. In that case, a U.S. non-resident return is usually required.

U.S. Employment or Business Income

Work performed in the United States, U.S. business activity, or other effectively connected income may require a U.S. federal non-resident return.

State Tax Returns

State tax filings may also apply. This can happen when a taxpayer has state-source income, rental property, employment income, or a part-year state residency issue.

Dual-Status and Move-Year Tax Returns

A person may need a dual-status tax return in the year they arrive in or leave the United States. In that year, the taxpayer may have both a resident period and a non-resident period for U.S. tax purposes.

The resident-period return generally reports worldwide income for the period of U.S. residence. By contrast, the non-resident period generally focuses on U.S.-source income.

The U.S.-Canada tax treaty may also affect the filing position in a move year. Therefore, taxpayers should review move-year filings carefully before preparing the return.

Common Non-Resident Filing Issues

Non-resident tax filing becomes more complex when the taxpayer has income in both countries, withholding at source, rental property, state or provincial filing issues, or a move during the year.

- Determining whether tax rules treat a taxpayer as resident or non-resident

- Reviewing Canadian Part I and Part XIII tax issues

- Preparing Canadian Section 216 rental returns

- Preparing Canadian Section 217 pension election returns

- Reviewing Canadian non-resident withholding tax

- Preparing U.S. Form 1040-NR filings

- Reviewing U.S. FDAP and effectively connected income

- Preparing U.S. rental income elections and reporting

- Reviewing state or provincial filing obligations

- Handling move-year or dual-status tax filing issues

What Happens Next

Non-resident filing situations vary widely. Therefore, the first step is to understand where you live, where the income is sourced, what tax was withheld, and whether any elections or treaty rules may apply.

Initial review

- We review your residency and move-year facts

- We identify the income source and filing country

- We consider withholding, treaty, and election issues

- We flag obvious prior-year or cross-border filing concerns

Next steps

- We explain which non-resident filings may apply

- We coordinate Canadian and U.S. filings where needed

- We prepare the relevant returns and supporting schedules

- We help you understand the filing process before submission

Frequently Asked Questions

Do non-residents always need to file a tax return?

No. In some cases, withholding tax may satisfy the filing obligation. However, the taxpayer may still need or benefit from filing a return depending on the type of income, country, and applicable election.

What is a Canadian Section 216 return?

A Section 216 return is a Canadian non-resident return for rental income. It can allow the taxpayer to report net rental income instead of being taxed only through gross-rent withholding.

What is a Canadian Section 217 return?

A Section 217 return may apply to certain Canadian pension, retirement, or benefit income paid to a non-resident. In some cases, it can reduce the final Canadian tax cost.

When does a Canadian need to file Form 1040-NR?

A Canadian may need to file Form 1040-NR if they have certain U.S.-source income, U.S. rental income, effectively connected income, or other U.S. non-resident filing obligations.

Do U.S. citizens in Canada file Form 1040-NR?

Usually no. U.S. citizens and green card holders generally file U.S. resident returns even while living in Canada. Form 1040-NR generally applies to non-resident aliens, not U.S. citizens.

What is a dual-status return?

A dual-status return may apply in the year a person becomes or ceases to be a U.S. tax resident. The return generally separates the resident portion of the year from the non-resident portion.

Official Government Resources

For official guidance, you can also review the following government resources:

- CRA information for non-residents and individuals leaving or entering Canada

- CRA Form T1159 for non-residents and deemed residents of Canada

- IRS information for nonresident aliens

- IRS information about Form 1040-NR

Need Help With a Non-Resident Tax Filing?

If you have income, property, residency changes, or filing obligations across the U.S.-Canada border, consider reviewing the correct filing approach before submitting a return.

We can help identify the required filings, prepare the relevant returns, and coordinate Canadian and U.S. reporting where needed.

Disclaimer: This page provides general information only and does not constitute legal, tax, accounting, investment, or financial advice. Non-resident tax filing obligations depend on the specific facts, residency status, income source, withholding, elections, treaty positions, prior filings, and applicable law. Therefore, obtain advice based on your own circumstances before taking action.