PFIC and Form 8621 Reporting for U.S. Citizens in Canada

Many U.S. citizens and green card holders living in Canada are surprised to learn that ordinary Canadian investments can create complex U.S. tax reporting issues.

Canadian mutual funds, Canadian ETFs, high-interest savings ETFs, pooled funds, and certain other non-U.S. investment products may be classified as Passive Foreign Investment Companies, commonly referred to as PFICs, for U.S. tax purposes.

PFIC reporting can be complicated. The issue is not only whether investment income was reported. PFICs may require IRS Form 8621, special tax calculations, basis tracking, and careful coordination with Canadian tax slips and brokerage records.

Need help reviewing Canadian investments for PFIC exposure?

We can help identify the issue, organize the records, evaluate the available reporting methods, and prepare a clear compliance plan.

Why PFICs Are a Common Problem for U.S. Persons in Canada

Many Canadian residents invest in Canadian mutual funds or ETFs without concern. For U.S. tax purposes, however, many non-U.S. pooled investment vehicles can fall under the PFIC rules.

This issue commonly affects:

- U.S. citizens living in Canada

- Green card holders living in Canada

- U.S. persons with Canadian non-registered investment accounts

- U.S. persons holding Canadian ETFs, mutual funds, or robo-advisor portfolios

- Taxpayers with TFSAs, RESPs, FHSAs, or other Canadian accounts invested in pooled funds

- Taxpayers whose prior U.S. returns did not include Form 8621

A Canadian brokerage statement or T3 slip usually does not warn you that an investment may be a PFIC. Many taxpayers only discover the issue years later.

What Is a PFIC?

A PFIC is generally a non-U.S. corporation that meets certain passive income or passive asset tests under U.S. tax rules. Many non-U.S. investment funds can fall into this category because they primarily hold passive assets or generate passive investment income.

For U.S. persons in Canada, PFIC issues often arise with the following types of investments:

Not every Canadian investment is automatically a PFIC. Individual shares of ordinary operating companies, for example, are not automatically PFICs merely because they are Canadian. The issue is most common with pooled investment products, and certain foreign REIT or real-estate fund structures may also need to be reviewed.

Why Form 8621 Matters

Form 8621 is the IRS form used by U.S. shareholders of PFICs for certain reporting, elections, income inclusions, distributions, and dispositions.

Depending on the facts, Form 8621 may be needed to report:

- PFIC ownership

- A QEF election

- Mark-to-market reporting

- Section 1291 excess distributions

- Gains on sale

- Annual income inclusions

- Basis adjustments

- Late or catch-up reporting

PFIC reporting becomes especially difficult where a taxpayer owns multiple funds, reinvests distributions, sells partial holdings, switches reporting methods, or has missing historical records.

Small PFIC Reporting Exceptions

There are limited de minimis exceptions that may reduce Form 8621 reporting for small PFIC holdings, but these rules are often misunderstood. They are not a general exemption from the PFIC rules.

Under the current IRS Form 8621 instructions, a shareholder may not need to complete the annual information section of Form 8621 for a specific section 1291 PFIC if total PFIC holdings are $25,000 or less at year-end, or $50,000 or less for a joint return, and there was no excess distribution and no gain from a sale or other disposition of that PFIC during the year.

A separate $5,000 exception may also apply to certain indirect PFIC interests where the shareholder's proportionate share of a specific section 1291 PFIC is $5,000 or less.

These exceptions generally do not apply where the taxpayer sold PFIC shares, received an excess distribution, needs to make a QEF or mark-to-market election, has annual QEF or MTM income reporting, or is correcting prior-year PFIC reporting.

For U.S. persons in Canada, the practical point is that even small Canadian mutual fund, ETF, or pooled fund holdings should still be reviewed carefully. The de minimis rules may reduce filing in simple low-value situations, but they do not eliminate the need to identify PFIC investments and determine whether Form 8621 is required.

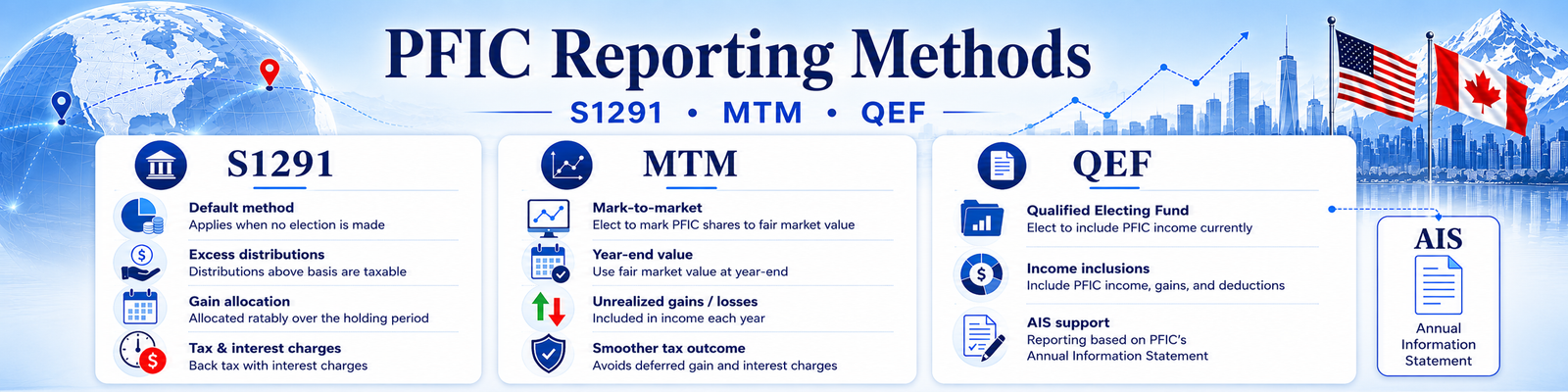

PFIC Reporting Methods

There are three common PFIC reporting approaches. The appropriate method depends on the investment, available fund information, election history, and prior-year reporting.

| Method | Typical Use | Common Issues |

|---|---|---|

| Section 1291 default rules | Generally applies by default where PFIC reporting applies and no valid QEF or mark-to-market election is in place. It may also be relevant where no historical Form 8621 reporting was done and no deemed-disposition or purging election has been made. | Can involve excess distributions, gains on sale, prior-year allocations, interest charges, and tax at prior-year rates. |

| QEF election | May be available where the fund provides a suitable PFIC Annual Information Statement. | Requires annual reporting of ordinary earnings and net capital gain, together with basis tracking and reconciliation to Canadian records. |

| Mark-to-market election | May be available for certain marketable PFIC stock, including some publicly traded PFIC shares, ETFs, mutual funds, or other regularly traded fund interests where the marketability requirements are met. | Can require annual fair market value reporting and may create taxable income without a sale. |

Why Canadian Tax Slips May Not Match PFIC Reporting

Canadian tax reporting and U.S. PFIC reporting often do not match.

A Canadian T3 slip may report taxable income under Canadian rules, while a PFIC Annual Information Statement may report ordinary earnings, net capital gain, or cash distributions under U.S. PFIC rules.

Differences may arise because of different tax rules, different fiscal year ends, timing differences, reinvested distributions, return-of-capital treatment, foreign exchange conversions, or differences between actual cash distributions and PFIC-reported amounts.

PFIC Basis Tracking

PFIC basis tracking is often one of the most important parts of the analysis.

Depending on the reporting method, basis may be affected by original purchase cost, reinvested distributions, QEF inclusions, actual distributions, mark-to-market inclusions, partial sales, foreign exchange rates, return of capital, and prior-year reporting errors.

A clean PFIC workbook is often just as important as the tax form itself.

How We Help

We help U.S. citizens, green card holders, and other U.S. persons in Canada identify, analyze, and organize PFIC reporting issues.

Depending on the engagement, we can assist with:

- Identifying which investments may be PFICs

- Reviewing available PFIC reporting methods

- Determining whether QEF, mark-to-market, or section 1291 treatment may apply

- Organizing Form 8621 reporting information

- Preparing PFIC income, distribution, gain, and basis workpapers

- Reconciling Canadian T3/T5/T5008 slips to U.S. reporting

- Reviewing prior-year PFIC omissions

- Coordinating PFIC reporting with FBAR, Form 8938, and T1135 issues

- Supporting taxpayers, CPAs, tax preparers, and financial advisors with PFIC matters

Documents Commonly Needed

The documents needed depend on the facts, but may include:

Investment records

- Year-end brokerage statements

- Transaction history

- Purchase and sale confirmations

- Dividend and distribution history

- Fund names and ticker symbols

- PFIC Annual Information Statements, if available

Tax records

- T3, T5, T5008, and other Canadian tax slips

- Prior U.S. and Canadian tax returns

- Prior Forms 8621, if any

- FBAR, Form 8938, and T1135 filings, if any

If records are incomplete, we can help identify what is missing and what may need to be reconstructed.

Common PFIC Warning Signs

You may need a PFIC review if:

- You are a U.S. citizen or green card holder in Canada

- You hold Canadian ETFs or mutual funds

- You use a Canadian robo-advisor portfolio

- You receive T3 slips from Canadian funds

- Your U.S. return reports foreign dividends but no Form 8621

- You sold Canadian funds without a PFIC calculation

- Your prior preparer did not discuss QEF, mark-to-market, or section 1291 treatment

- You are considering Streamlined filing or another late-compliance process

Frequently Asked Questions

Do all Canadian ETFs and mutual funds create PFIC issues?

Not every Canadian investment is automatically a PFIC, but many Canadian ETFs and mutual funds may be PFICs for U.S. tax purposes. Each investment should be reviewed based on the fund structure and available information.

If I reported the income in Canada, do I still need Form 8621?

Possibly. Canadian tax reporting does not eliminate U.S. PFIC reporting. A Canadian T3 or T5 slip may report income for Canadian purposes, but U.S. PFIC reporting can require separate Form 8621 analysis.

If I reported the dividends on my U.S. return, is that enough?

Not necessarily. Reporting dividends may not satisfy PFIC reporting if Form 8621 was required.

What is the difference between QEF, mark-to-market, and section 1291 reporting?

QEF reporting generally uses annual fund-provided information. Mark-to-market reporting may be available for certain marketable PFICs and uses annual fair market value changes. Section 1291 is the default regime and can involve excess distribution and interest-charge calculations.

What if the fund provides a PFIC Annual Information Statement?

A PFIC Annual Information Statement may make QEF reporting possible, but the information still needs to be reviewed and reconciled to actual distributions, Canadian tax slips, and basis tracking.

What if I sold a PFIC?

A sale can trigger special PFIC calculations. Depending on the reporting method, the gain may not be reported as a simple capital gain.

Can prior-year PFIC problems be fixed?

Sometimes. The best approach depends on the facts, including whether prior returns were filed, whether income was reported, whether forms were omitted, and whether the taxpayer is considering amended returns, Streamlined filing, or another compliance path.

Official IRS Resources

For official U.S. tax guidance on PFIC and Form 8621 reporting, you can also review these IRS resources:

- IRS information about Form 8621

- IRS Instructions for Form 8621

- IRS Form 8621 PDF

- IRS information about Form 8621-A for certain late PFIC elections

- IRS Notice 2014-51 on Section 1298(f) PFIC annual reporting

- IRS prior-year Form 8621 forms and instructions

Need Help With PFIC or Form 8621 Reporting?

If you are a U.S. citizen, green card holder, or other U.S. person in Canada and you own Canadian ETFs, mutual funds, or other pooled investments, it is worth reviewing whether PFIC reporting applies.

We can help identify the issue, organize the records, evaluate the available reporting methods, and prepare a clear compliance plan.

Disclaimer: This page provides general information only and does not constitute legal, tax, accounting, investment, or financial advice. PFIC reporting depends on the specific facts, investments, account types, prior filings, and available fund information. You should obtain advice based on your own circumstances before taking action.